YWR: The Great Front-Run

www.ywr.world

Disclosure: Personal views only. Not investment Recommendations

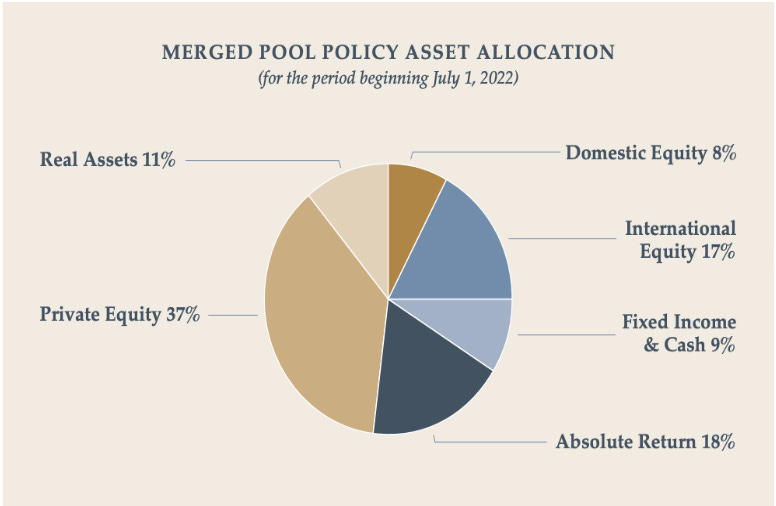

It started with the Stanford Endowment. I was curious how the smartest people in the room (and I’m not using air quotes) invest their money for the long term. Their returns and investments have been legendary (11% annualised for 30 years). …